SBF’s Side of the Story

Sam Bankman-Fried is serving 25 years for allegedly defrauding FTX customers of $8 billion. But now that they’re being repaid with interest, the question arises: Was guilt really proven beyond reasonable doubt? Or was the truth buried by a media frenzy, conflicted bankruptcy lawyers, and a political war on crypto?

I knew little about SBF before his trial. But after 1,000 hours of research, I found a story far more complex — and troubling — than what the public was told.

#FreeSBF

-

In 2017, 25-year-old Sam Bankman-Fried (SBF) co-founded a hedge fund called Alameda Research that traded in crypto. In 2019, SBF co-founded a crypto exchange — a platform for bringing together buyers and sellers of crypto — called FTX. In 2021, he handed over the running of Alameda to his sometime-girlfriend Caroline Ellison and her co-CEO, although he continued to own 90% of Alameda.

Alameda was one of the hedge funds that traded on FTX and provided the exchange with liquidity. FTX was a margin exchange — it allowed customers to trade with funds borrowed from other customers.

Within three years of its founding, FTX had grown to become the world’s second-largest crypto exchange. It was valued at $32 billion.

In November 2022, an Alameda balance sheet leaked by an unidentified source and a tweet from rival crypto exchange Binance cast doubt on the financial health of Alameda and FTX, triggering both a 50% crash in the value of Alameda’s assets and a run on FTX deposits. The amount FTX had on hand was short billions of dollars. It halted withdrawals, and soon after declared bankruptcy.

All margin exchanges are vulnerable to liquidity crises, and neither poor risk management nor bankruptcy are crimes. But rumor quickly spread that criminal activity had contributed to FTX’s collapse. In December 2022, the CFTC alleged that FTX had “irrevocably lost” over $8 billion of customer funds.

Later that month, U.S. prosecutors charged him with fraud and conspiracy; he was arrested and later extradited to the U.S. In August 2023, he was sent to MDC Brooklyn, his bail revoked for alleged witness tampering.

Caroline Ellison and FTX executives Gary Wang and Nishad Singh took plea deals and testified against SBF in October 2023. The verdict was guilty on all seven counts: two counts of wire fraud (on customers and lenders) and five counts of conspiracy (to commit wire fraud on customers and lenders, securities fraud on investors, commodities fraud on customers, and money laundering).

On March 28, 2024, SBF was sentenced to 25 years in prison and ordered to pay $11 billion in forfeiture to the U.S. government.

In 2025, repayments began, with customers receiving 100% of their dollarized claims plus 9% annual interest.

SBF continues to maintain his innocence and has appealed his conviction.

-

SBF is alleged to have stolen $8+ billion from FTX customers, and then lied about it to equity investors in FTX and to lenders to Alameda. According to the U.S. government, SBF repeatedly represented that customer funds were “safe,” while he secretly:

Allowed Alameda to spend unlimited amounts of other customers’ funds via a backdoor in its customer account on FTX

Directed customers to deposit funds into bank accounts controlled by Alameda and told Alameda to spend those funds

FTX, prosecutors argued, was a scam from the start. It “had more debts than assets” from 2021, customer liabilities became “unrepayable,” and “there is no serious dispute that around $10 billion went missing” (trial transcript) — all spent on personal luxuries, reckless investments, repaying loans, and secret political influence to help SBF steal even more.

For an overview of the government’s version of events in its own words, see the 18-page indictment, pages 18-29 of the reply to SBF’s appeal, or the following short summary from the website of the Department of Justice:

“Bankman-Fried was the founder and chief executive officer of FTX, an international cryptocurrency exchange. From 2019 to 2022, Bankman-Fried was the leader and mastermind of a scheme to defraud customers of FTX by misappropriating billions of dollars of those customers’ funds. Bankman-Fried took FTX customer funds for his personal use, to make investments and millions of dollars of political contributions to candidates from both parties, and to repay billions of dollars in loans owed by Alameda Research, a cryptocurrency trading fund that Bankman-Fried also founded. Bankman-Fried also defrauded lenders to Alameda and equity investors in FTX by providing them false and misleading financial information that concealed his misuse of customer deposits.

“Bankman-Fried repeatedly told his customers, his investors, and the public that customer deposits into FTX were kept safe and were held in custody for the customers, that customer deposits were kept separate from company assets, and that customer deposits would not be used by FTX. He also repeatedly claimed that his trading company, Alameda, did not have any privileged access to FTX and did not receive special treatment from FTX. Those statements were false, and Bankman-Fried in fact channeled billions of dollars in customer deposits from FTX to Alameda, and then used those funds to make investments for his own benefit, to make political contributions, and to spend on real estate, among other expenditures. He employed a variety of fraudulent means to perpetrate this fraud. For instance, Bankman-Fried directed co-conspirators to alter FTX’s computer code to allow Alameda to withdraw effectively unlimited amounts of cryptocurrency from the exchange and made false statements to financial institutions to conceal his misuse of customer dollar deposits. He also directed the creation of false financial statements for Alameda’s lenders, inflated FTX’s revenues and profits in numbers provided to investors, and backdated contracts and other documents to conceal his fraudulent conduct.”

❖ CORE DEFENSE ❖

FTX was a real, innovative business run in good faith. Alameda, SBF’s trading firm, borrowed from FTX just as any margin customer could, with special access that was legitimate and known to many. Shortly before the collapse, SBF learned that Alameda’s balance on FTX had become net negative, and he began trying to fix it.

But Alameda and FTX always had more assets than liabilities overall. If their lawyers hadn’t put them in bankruptcy, customers would likely have been fully repaid in kind within weeks of the run on the exchange, and FTX would be worth close to $100 billion today.

Read on for details…

“The core dispute in this case is whether the defendant knew taking the money was wrong.”

“[G]ood faith on the part of a defendant is a complete defense to the charge of wire fraud.”

THE ACCIDENT: ALAMEDA INVESTS $8 BILLION OF CUSTOMER FUNDS

If Alameda “used” $8 billion of customer deposits at SBF’s direction, why did no one testify that he knew about it until the weeks before the run on FTX — and why did witnesses say he immediately tried to reverse it and even proposed shutting Alameda down?

Alameda invested around $8 billion of customer fiat (i.e. non-crypto) deposits into illiquid assets — assets that couldn’t be quickly sold without losing significant value. SBF only learned about this after it had happened, piecing it together over June to October 2022.

-

In June 2022, SBF and co-defendants Ellison, Wang, and Singh discovered that Alameda hadn’t transferred the fiat deposits it had been collecting for FTX, even though FTX had opened its own bank accounts months earlier. “[I]nitially, FTX didn't have its own bank accounts, so it used Alameda bank accounts” (Wang testimony); “by 2022, . . . FTX was no longer using Alameda bank accounts . . . [b]ut . . . the fiat@ liability still exist[ed]” (Wang testimony). They calculated that “in banks, Alameda's or FTX, there should be $11 billion of fiat sent by customers” (Singh testimony). In other words, Alameda still owed FTX up to $11 billion.

“[I]n the months following June 2022, there was a project . . . that included getting a clearer picture of the fiat@ liability that was owed by Alameda” (Wang testimony). Rather than keeping the liability a secret, SBF looped in more people to work out its exact size: “Adam, Andrea, and Gary [Wang] went through an exercise with help of the fiat settlement team to . . . split that fiat@FTX.com balance into two balances: One corresponding to what Alameda owed, one corresponding to what FTX owed” (Singh testimony).

In September 2022, Ellison revealed that Alameda would not be able to transfer the amount it owed FTX quickly because Alameda had invested it all into assets with low liquidity. “[N]ot all elements of the prosecution narrative line up neatly. Singh said he left the crucial June meeting still thinking things were OK and did not realise customer funds were being raided until September” (Financial Times). “The majority of the liability consisted of FTX customer fiat that was supposed to be housed in Alameda bank accounts, and nothing about the [June 2022] exercise suggested to Nishad that those funds were not in the bank accounts[;] Ellison had even confirmed months earlier that Alameda was tracking this fiat liability” (Singh sentencing memo). “[O]n September 7, . . . Ellison tells [Singh], Gary [Wang], and the defendant over a Signal chat that it is impossible to close out Alameda's borrowing because of the size of the hole [i.e., liquidity gap]” (prosecutor, trial transcript).

This was news to SBF. “What I [had] believed was that either the funds were just being held in a bank account and, you know, not used or removed, or that they were being sent to FTX in one way or another, maybe as stablecoin, or to the extent that those weren't happening and that Alameda was borrowing funds and using them, that that would be reflected as a borrow on Alameda's info@ account . . . that I had looked at[, which] was Alameda's primary trading account on FTX” (trial transcript).

In October 2022, SBF confirmed the size and illiquidity of the liability for himself. “I ultimately learned confidently that the fiat@ liability, in particular its size, was 8 billion from a database. . . . In around September and October of 2022, FTX's developers had built a second database . . . to have a source that nondevelopers [like SBF] could interact with. . . . I got access in October of 2022” (trial transcript). “By October, [SBF] had a clearer picture. It was only then that he could see that Alameda had been operating as if the $8.8 billion in customer funds belonged to it” (Going Infinite).

No testimony or evidence suggested that SBF had instructed Alameda to touch any of these fiat funds. Indeed, “no one testified that they knew about this liability, which we've come to learn was related to the fiat@ account, before June 2022” (defense counsel, trial transcript).

-

Part of the explanation may be that the accounting at Alameda was chaotic:

“Q. By mid-2022 . . . Was Alameda also still borrowing money from FTX? A. Yeah. . . . Q. Were you keeping track of that borrowing? A. Yeah. Not necessarily carefully, but to some extent” (Ellison testimony).

When asked if the spreadsheet Ellison made for SBF in the fall of 2021 for “analyzing Alameda's NAV . . . account[ed] for the customer money Alameda was already using that came in the form of customer fiat or dollar deposits”, Ellison replied, “I don't recall exactly how they accounted for that, like whether that's included in the current totals or not” (trial transcript).

“Q. . . . So if Sam wanted to see the account balances of any customer on the FTX exchange, he could call up that information on the admin user's dashboard, right? A. Yes. Q. And he could do that for Alameda, for example. A. Yes. . . . Q. Okay. But as you said, the fiat@ liability was not part of Alameda's balances on the admin user's page; is that right? A. Not as of June 2022” (Wang testimony).

“[Ellison] wasn't aware that there was a bug in [Alameda’s] system for six months after it had already been discovered, and she woke up one day and [mistakenly] believed that her company, which previously had a NAV of 8 to 10 billion, was now bankrupt, overnight” (defense counsel, trial transcript).

“[Ellison] testified that the firm had attempted to hire several people to oversee Alameda’s accounting, but they all left” (CNBC).

But even if Ellison understood what was happening all along, by 2022, she was calling the shots at Alameda and SBF was paying little attention: “Ellison testified that she and Trabucco began handling a lot of Alameda’s day-to-day business as early as 2020, well before officially taking over, and that there were periods of time where Bankman-Fried would not talk to them much. By 2021, she testified, Bankman-Fried had largely stopped coming into the Alameda office and had left more of the job to Ellison. . . . Ellison also testified that Bankman-Fried had discussed adding a new co-CEO when Trabucco left, but she resisted. . . . Ellison said she was skeptical [about SBF’s advice to hedge] and didn’t do anything about it. . . . Ellison said [her and SBF’s] breakup in the spring of 2022 affected communications between the two of them” (CNBC). Ellison even wrote in her journal in April 2022, “I almost feel like I'm living a lie because people don't realize how little I'm working and what a shitty job I'm doing” (Ellison sentencing memo).

-

“I f—ed up.”

— SBF, draft congressional testimony

The miscommunication over the fiat deposits was undeniably a major f—up. But SBF appears to have reasonably believed this wouldn’t put customers at any serious risk for three reasons: Alameda’s net asset value (NAV) was still $8-10 billion, there was still enough liquidity to meet 50x typical daily withdrawals, and there’d been no clear violation of any laws or terms.

SBF says he checked that Alameda’s overall assets still exceeded its liabilities by $8-10 billion: “I asked Caroline to confirm that this definitely meant that Alameda's NAV was positive 8 to 10 billion . . . and she said that they had in fact confirmed that” (trial transcript). SBF also owned 60% of FTX — valued at $32 billion earlier in the year — which ultimately helped secure a $4 billion liquidity offer when withdrawals unexpectedly spiked. (There was also an informal offer of $2-4 billion and plausibly SBF would have attracted even more offers if given a few more days; the bankruptcy team, however, ignored all offers of liquidity.) After Ellison revealed the $8 billion mismatch between the liquidity that might be needed in an emergency and what was available, SBF reportedly said, “‘I'm not sure what there is to worry about. NAV is fantastic by almost any measure. It was super positive even if you don't include FTX and FTX.US equity’” (Singh testimony). And when asked to “name any customers that were allowed to pledge outside investments as collateral for withdrawing money on FTX apart from Alameda,” SBF replied, “I believe that we did that with a firm called Crypto Lotus, and I believe that we considered that with Three Arrows” (trial transcript).

Customer withdrawals were typically “around a hundred million per day” (Wang testimony). Despite Alameda having put $8 billion of deposits into illiquid assets, SBF calculated that “in 24 hours, if pressed, I think we could deliver around $5 billion” in withdrawals (Singh testimony) — which they did, in fact, end up managing.

FTX operated a margin lending program, which allowed customers to borrow from one another. (Participants were warned it was “HIGH RISK,” especially since “even if you have not suffered any liquidations or losses, your Account balance may be subject to clawback due to losses suffered by other Users” (terms of service), and that “[w]hile FTX aims to reduce the likelihood of clawbacks, they are still possible” (FTX blog).) There appear to have been enough of these margined assets to cover Alameda’s $8 billion “borrow” — when FTX filed for bankruptcy, it owed non-margin customers $2.03 billion, and FTX and Alameda had sufficient liquid funds to pay them back. Indeed, according to the defense’s expert witness, “80 percent of the assets on FTX were margined assets . . . 80 percent are in this margin trading where customers are always borrowing other customers' assets” (defense counsel summarizing Dr Pimbley’s testimony). But even if one were to insist that it was not appropriate to categorize this $8 billion error as a margin borrow, it was also true that — as bankruptcy filings acknowledge — “[t]he user agreements [] did not provide for the segregation of assets or the return of assets in specie to customers[, n]or did such ‘ownership’ language cover the billions in fiat currency owed to customers” (court docket).

Consequently, “Sam said he's not too worried and he described a number of sort of strategies [to raise liquidity] . . . . He described selling off Alameda's illiquid but, according to his estimation, valuable assets, and properties; he described, for the ones that weren't sellable but generated revenue, making sort of low-hanging changes to make them more profitable; he discussed raising from investors, selling FTX equity . . . I asked if now, Sam would take seriously cutting expenses . . . He said yes” (Singh testimony).

To reduce the risk of something like this happening again, SBF “asked Andrea Lincoln, one of the developers, to work on [getting their accounting in shape], with an ETA of October 15th” (defense counsel, trial transcript). And in September 2022, he “laid out a case for shutting down Alameda, citing that Sam didn't have faith in its——the competency of its leadership without him more involved” (Singh testimony). “The defendant wrote a five-page memo that includes six numbered points for why to shut down Alameda,” (prosecutor, trial transcript); “if he really thought Alameda was the key to his fraud, if this was the engine to keep stealing money from customers, the last thing he would do would be to propose shutting it down,” (defense counsel, trial transcript).

THE DISTRACTION: BACK DOORS & BANK ACCOUNTS

If business practices like the banking setup and ‘back door’ borrowing were unlawful, why did so many people know about them?

“Now, the defendant set up two secret ways through which Alameda could take or borrow customer money . . . by withdrawing it from FTX from its cryptocurrency wallets in unlimited amounts, and by taking it out of the bank accounts that received those customer deposits. . . . [T]he defendant was treating their deposits as his personal piggy bank by funneling that money to Alameda” (prosecutor, trial transcript).

“FTX was a relatively rare example of a crypto company that did have a full audit under generally accepted accounting principles. . . . Prager Metis said it stands behind its audit opinion. . . . Armanino is ‘confident that it complied with all applicable professional standards in the conduct of its audit work’” (Wall Street Journal).

-

At trial, the government portrayed FTX’s banking structure as a mechanism purposefully designed for stealing funds: “[T]he money never actually made it to FTX. Instead, the defendant opened a bank account that was under the control of Alameda, his other company. He put the information for that Alameda bank account on FTX's website as the place where customers should send their money. So when customers thought their money was going to the exchange, they were actually sending their money right into the defendant's pocket. You will hear that the defendant even lied to a bank to set up an Alameda bank account that he used for this” (prosecutor, trial transcript).

But the U.S. government’s war on crypto was the real reason this banking setup ever existed. During Biden’s covert efforts to debank the industry, crypto exchanges struggled to get their own bank accounts, often having to rely on payment processors to allow customers to buy crypto using fiat currency like U.S. dollars. FTX initially had an Alameda-owned bank account accept customer fiat deposits on its behalf, along with “multiple other payment processors for FTX [who] had accounts on FTX as well” (trial transcript).

As one observer puts it, “the primary reason funds were comingled stems from the Biden administration’s refusal to allow companies like FTX access to traditional banking services[, which] forced Bankman-Fried to move money through his hedge fund, an act that, while improper, was a direct result of systemic barriers” (amuse).

SBF was barely even involved in this process. “FTX began receiving deposits into [Alameda’s bank account]. [SBF] says he learned about it later, sometime in 2020” (Bloomberg). “Bankman-Fried says the decision to incorporate [this new bank account] was communicated by Dan Friedberg” (Bloomberg). One of SBF’s co-defendants said that lawyers helped implement this structure and that, far from the bank being “lied to,” it was actually the bank’s idea. (Email screenshots confirm that the bank was at the very least aware of the arrangement.)

It was not particularly hidden from customers either. FTX’s wire instructions for fiat deposits said, “Beneficiary Name: Alameda Research LTD” (X).

-

Putting the $8 billion fiat accident in 2022 aside, Alameda’s overall account balance was always positive on FTX. As a margin customer, it borrowed and withdrew funds from the exchange, while posting more in collateral than it borrowed. Unlike with the bank account, this other “secret way[] through which Alameda could take or borrow customer money” did not involve net borrowing.

As SBF explained at trial, with FTX’s margin lending facility, “[s]o long as we believed that the risk was being managed, which is to say, so long as we believed its assets were greater than its liabilities, we didn't care if the user, you know, withdrew funds and used them to buy muffins, to pay business expenses, to invest or anything else” (Guardian). This is consistent with pre-bankruptcy statements: “You can deposit, and withdraw, and trade, as long as you don't go beyond your margin limits” (X). “Reminder: on FTX, all margin/leverage/futures/etc. are automatic. . . . You can even withdraw short!” (X). “You can even do this with withdrawals!” (Spot Margin Trading Explainer, FTX.com).

Prosecutors emphasized that one of Alameda’s subaccounts was “[n]egative $2.7 billion” in June 2022 (trial transcript). However, Wang confirmed on cross-examination that when the up-to-$11-billion fiat liability was put aside, Alameda’s net balance on FTX was positive: “The numbers on the spreadsheet reflect about 11 billion liability for fiat and almost a total of 11 billion liability on the exchange, right? A. Yes” (trial transcript). According to SBF, Alameda was borrowing — again, putting the fiat ‘borrow’ aside — “millions in 2019 . . . and then by 2022, my understanding was that it was around $2 billion on average of borrowing” from FTX, maintaining a balance that was “[o]verall positive, but negative in some assets” (trial transcript). Similarly, Singh said that prior to Ellison telling him in September 2022 that she’d invested the fiat deposits, he “thought Alameda had positive balances on FTX, that it was borrowing lots in some places but that overall they had more money than they didn't” (trial transcript).

Singh further said that everyone at Alameda must have known that one of its subaccounts on FTX was negative $2.7 billion: “This number . . . is a front-and-center number in all of Alameda's trading systems . . . [which] I couldn't imagine being missed or ignored by anyone there” (trial transcript).

-

Alameda’s customer account on FTX had what the media dubbed a ‘back door’ — certain subaccounts had the auto-liquidation feature turned off, and one used $3 billion of a $65 billion credit line (“[there was] around $3 billion . . . in borrowing against the line of credit of 65 billion” (Wang testimony)). But as we’ve just seen, Alameda’s customer account was posting more assets to FTX than it was borrowing from it. So why the ‘back door’?

As a backstop liquidity provider, Alameda “agreed to buy assets that are held by users whose accounts are losing too much money” to “protect[] the rest of the FTX customers from incurring losses” (Wang testimony). As a market maker, it maintained a vast number of open orders to support market liquidity. But the system counted these unfilled orders against Alameda’s collateral, making it look like Alameda didn’t have enough left to safely take on new trades — even when it actually did. During times of platform stress, the system might then block Alameda from absorbing liquidated positions, forcing unwanted trades onto other customers instead.

This was not a hypothetical concern. “[FTX’s] automated ‘risk engine’ suffered an error that turned a routine liquidation of a few thousand dollars into an almost catastrophic series of trades. . . . As FTX grew, the volume of trades strained the company's computer systems . . . The trading became so large, it had to go to a backstop liquidity provider, in this case Alameda” (CNN). “That, in turn, caused Alameda's account to go under water because of the positions it was being handed in the trillions of dollars and triggered a potential liquidation of Alameda's account which . . . ultimately would claw back funds from the entire platform's users” (SBF testimony). Alameda had stopped being eligible as a backstop liquidity provider since “its free collateral was zero [—] not because it had a bunch of positions but because it had tons and tons of open orders out——open orders for the purpose of providing liquidity on the hundreds of markets” (Singh testimony).

The solution? Replace automated risk checks on Alameda’s customer account with manual monitoring. Asked what was done in response to the near-catastrophic liquidation, Singh pointed to the idea of “increasing Alameda's line of credit” and the auto-liquidation exemption: “if the sole cause of Alameda being an ineligible backstop provider was that it didn't have enough free collateral, that was no longer considered . . . [which] would be helpful to customers” (trial transcript). Similarly, when Wang was asked about the goal of the huge credit line, he said it was to ensure “[i]t would not impact Alameda placing orders on the exchange for market making” and agreed that $65 billion “was just sort of a notional number to make sure that this problem of butting up against the ceiling didn't happen again” (trial transcript). (Why not $99,999,999,999? “Some have wondered why Wang chose such a seemingly arbitrary number as $65,355,999,994. My best guess is he meant to set it to around $65.535 billion . . . 65,535 [] is meaningful in computer science as the largest possible value of an unsigned 16-bit integer” (Molly White).)

Wang acknowledged that “Alameda wasn't the only customer on FTX to be exempted from auto-liquidation” (trial transcript) and, according to Singh, the exemption was “used by other developers, too, for legitimate purposes” (Singh sentencing memo). FTX’s three most senior lawyers also knew about it: “Q. . . . [I]n August of 2022 [] you learned about Alameda having certain privileges on the FTX exchange. . . . Did you discuss this with anyone else besides Mr. Dexter and Mr. Miller around that time? A. Yes. I discussed it with Dan Friedberg, Nishad, and Sam. And David. . . . [They decided to] change it to a delayed liquidation mechanism, make it known to our users and our regulators, and also offer it on a nondiscretionary basis to all large market makers. . . . Nishad had assured me that that mechanism had never been triggered” (testimony of general counsel Can Sun).

The so-called ‘back door’ was therefore irrelevant to what went wrong at FTX. It wasn’t built or used to siphon off funds, but to minimize customer losses.

THE FABRICATION: FTX WAS NEVER ACTUALLY BANKRUPT

If SBF had more debts than assets for at least a year before FTX collapsed, why do bankruptcy court filings indicate the opposite?

“Billions of dollars missing in cryptocurrency, billions of dollars missing from bank accounts, and there is no serious dispute about that. . . . [T]he defendant schemed and lied to get money, which he spent, and now it's gone. . . . At this point [SBF is] already able to see in late 2021 that Alameda has more loans than it has assets. . . . [T]he defendant had more debts than assets and the only available money was this FTX customer money” (prosecutor, trial transcript).

“[G]iven the emerging picture of FTX’s finances, could it be that FTX didn’t have to go into this bankruptcy with a [b]illion-dollar price tag?” (American Prospect).

“So FTX was … illiquid but solvent? Absolutely wild” (Matt Levine, May 2024).

-

Now that customers are being made whole (potentially at current prices), many are quick to add that even if FTX’s assets exceeded its liabilities when it filed for bankruptcy — even if the $8 billion owed to customers was never in fact ‘missing,’ just temporarily tied up in various investments — this is irrelevant to the question of whether or not there was fraud.

Perhaps. But I include the ‘missing vs. illiquid’ question here because people seem to find it relevant when they think the answer reflects badly on SBF. “One key issue was how much money FTX’s customers lost. During the trial, the prosecution and its witnesses repeatedly – in fact, 97 times – put that number at $8 billion. Although no proof to substantiate this massive figure was ever offered, the prosecution clearly wanted it to stay in jury members’ heads” (Project Syndicate). Some wonder how the FTX story would have played out had this ‘irrelevant’ accusation never been part of it.

What’s more, while the prosecution was free to say to the jury, “Billions of dollars from thousands of people gone,” the judge prohibited the defense from arguing that customer funds were not, in fact, “gone,” or that the investments had done well (trial transcript). The defense had protested that “[while] the prosecution was trying to paint FTX’s investments as risky and bad, Anthropic’s success showed that their investments were merely part of a reasonable investing strategy,” but the judge ruled that “any success was irrelevant . . . and Anthropic . . . should not be discussed” (Wired). “The government hammered these points in closing, arguing Bankman-Fried had caused billions in losses—money that was ‘missing.’ It repeatedly argued FTX and Alameda were ‘deeply in the red,’ ‘$10 billion plus in the hole,’ and ‘totally under water.’ And it contended the insolvency was ‘very clear to the defendant.’ The defense was prevented from presenting evidence rebutting these arguments” (SBF’s appeal).

-

SBF has consistently maintained that FTX remained solvent — that it always had enough assets to meet its liabilities if given time to liquidate them — and that FTX US was always both solvent and fully liquid (SBF’s Substack).

Shortly before the bankruptcy, the tech team had confirmed that FTX US was unaffected by the liquidity crisis at FTX (a separate, non-U.S. entity with no U.S. customers). Ten months later, an Independent Examiner reached the same conclusion.

As for the international exchange, in the balance sheet SBF sent investors the day before it filed for bankruptcy, FTX “is recorded as having liabilities of $US8.9 billion” against “a total of $US9.6 billion of assets” (AFR). “Bankman-Fried [always] insisted that all the money was still somehow accessible . . . In some ways, his narrative appears to be proving true. . . . For FTX customers, being made whole, according to a judge’s ruling, means getting the cash equivalent of what their crypto was worth in November 2022” (CNBC). “Was SBF (sort of) right? It turns out, FTX lawyers now say it will be able to pay creditors in full” (Andrew Ross Sorkin). “FTX has estimated that it will have between $14.7 billion and $16.5 billion available to repay creditors, enough to pay customers at least 118% of the value in their accounts as of November 2022” (Reuters).

But SBF was not merely “in some ways,” “sort of” right. Commentators are fond of attributing FTX’s ability to repay customers to nothing more than a meteoric rise in the value of its investments and a Herculean effort by the bankruptcy lawyers. Few people are aware that those bankruptcy lawyers have produced public calculations of petition-date balances — the same lawyers who originally reported SBF to authorities, who strong-armed him into letting them file for bankruptcy, and who ultimately paid themselves and their associates $1.5 billion to manage the estate. And what do their own calculations show? On the eve of the bankruptcy, FTX had around $14 billion of assets against $9.2 billion of liabilities to customers. It was solvent.

-

This heavily conflicted team of lawyers have nonetheless repeatedly insisted that FTX was “hopelessly insolvent” (court docket), that FTX US “is not solvent” (congressional testimony), and that the situation would likely only worsen, with the “[r]ecoverable value [of the estate’s investments] likely to be materially lower than acquisition value” (presentation to creditors). They even sent a ‘victim impact statement’ to the trial court on the eve of SBF’s sentencing, stating — without evidence — that his claim that “FTX was solvent at the time that the Chapter 11 petition was filed . . . is categorically, callously, and demonstrably false” (court docket).

The judge believed them, arguing at SBF’s sentencing, “[F]or the reasons very well articulated by Mr. Rehn in the submission on behalf of the debtor's estate, even the premise that customers will be paid dollar-for-dollar for the dollarized losses as of the petition date is pretty speculative, even at this stage” (court docket).

Prosecutors believed them, describing to the jury how, as far back as 2021, SBF allegedly knew that “they've got more loans than assets, he sees they're in the red” (trial transcript).

The press believed them, reporting over and over again that around $8 billion had been lost: “FTX says it has identified a deficit of $8.9 billion in customer funds that it can’t account for, the first time the bankrupt cryptocurrency exchange has pinned down how much money has gone missing” (WSJ).

And customers believed them, some selling their claims for as little as three cents on the dollar. Today, claims are fetching up to 147%.

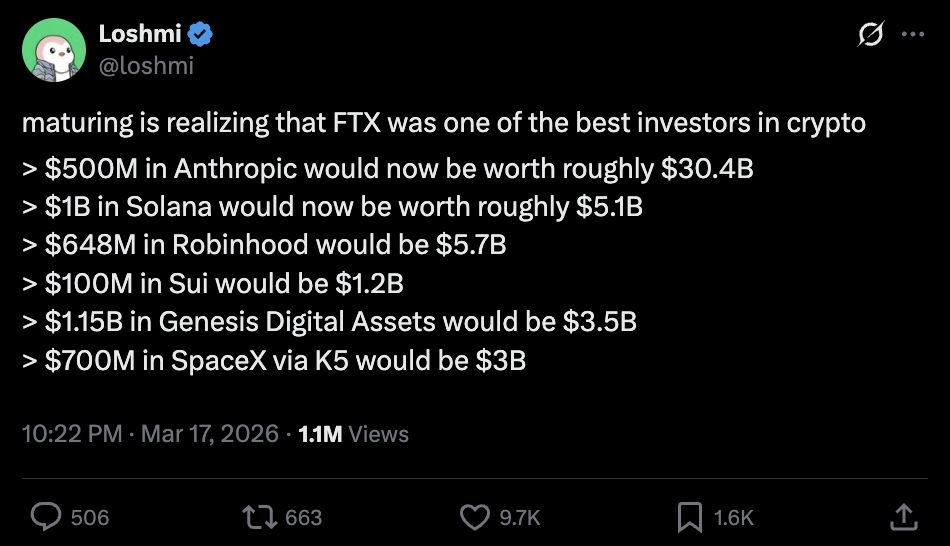

In fact, not only was there enough in November 2022 to fully repay customers — with seemingly enough liquidity on the way to process all repayments, in kind, that same month — there could easily have been enough to fully repay customers today, at today’s prices, several times over. In their sentencing letter, the bankruptcy lawyers characterized their work as “digging through the rubble of Mr. Bankman-Fried’s sprawling criminal enterprise to unearth every possible dollar, token or other asset that was spent on luxury homes, private jets, overpriced speculative ventures, and otherwise lost to the four winds” (court docket). But FTX’s Anthropic stake alone would be worth more today than the book value of the entire venture portfolio of 300+ investments at the time of the bankruptcy. The estate also missed out on huge gains from Solana, Sui, Cursor, Circle, Robinhood, Worldcoin, FTT, and the going-concern value of FTX itself. In March 2025, SBF estimated that, had the lawyers not placed FTX into bankruptcy, rather than sitting on $14.5 billion to $16.3 billion of assets today, FTX would have around $93 billion.

❖ 8 MORE DEFENSES ❖

-

“To prove intent to defraud, the government contended that certain FTX policies and business practices were deceptive. Bankman-Fried sought to show that the policies and practices were appropriate and had been adopted with counsel’s advice. . . . [T]he solution for [] potentially false testimony is cross-examination and contrary evidence, not exclusion. . . . Before trial, the district court ruled that all defense evidence on advice-of-counsel was inadmissible absent explicit advance approval by the court. It then rejected the defense’s detailed written proffer. Bankman-Fried was thus forced to sit for a deposition, allowing the government to cross-examine him before he took the stand—something that apparently has never happened before in federal court” (SBF’s appeal).

“[The judge] ruled that Bankman-Fried could offer limited testimony on the involvement of lawyers in creating FTX’s corporate document retention policy . . . [but] den[ied] Bankman-Fried’s efforts to obtain the document retention policy in discovery . . . and [] refus[ed] to allow cross-examination of the cooperating witnesses on the same topic” (SBF’s appeal). (“[SBF] says Chief Regulatory Officer Dan Friedberg put together a documentation-retention policy . . . [A]ny formal business communications, any decisions made and any records would not be deleted. . . . Bankman-Fried says in November 2022 he took an effort to disable auto-deletion ‘on any place I found it’” (Bloomberg). “Bankman-Fried testified that he was merely following a rule he picked up . . . at Jane Street. That was the ‘New York Times test,’ which, according to Bankman-Fried, was a frequent point of reference at the elite quant shop. ‘Anything that you write down,’ he recalled, ‘there's some chance it could end up on the front page of The New York Times.’ He added: ‘A lot of innocuous things can seem pretty bad’ without context” (CoinDesk).)

“The court excluded all the other proffered testimony. The court thus excluded evidence that (a) lawyers approved the North Dimension entities and bank accounts [Alameda’s bank accounts for receiving customers’ fiat]; (b) lawyers drafted the Payment Agent Agreement between FTX and Alameda; (c) lawyers approved loans from FTX to Bankman-Fried and others; and (d) lawyers drafted and approved FTX’s terms of service” (SBF’s appeal).

“FTX’s bankruptcy highlights how much power the debtors and their lawyers have in controlling the facts and the evidence. . . . SBF’s defense lawyers were stymied from mentioning the role of lawyers at FTX (except for one lawyer, Daniel Friedberg, who . . . had tried unsuccessfully to keep Sullivan & Cromwell from running the bankruptcy). . . . SBF’s lawyers tried to raise the name of Ryne Miller, the former Sullivan & Cromwell partner who was general counsel of FTX U.S.:

SBF’s lawyer: I wanted to ask him [an FBI agent who was testifying] if he knows who Ryne Miller is.

Judge Lewis Kaplan: You can ask him who Johnny Podres was.

SBF’s lawyer: Yes, your Honor.

Judge Kaplan: He was a pitcher for the Brooklyn Dodgers.

SBF’s lawyer: Nothing further.” (American Prospect)As one co-defendant put it, “But I don't know what the point of the lawyer is then. If I go to the lawyer and say, ‘Is this MTL legal or is this campaign finance thing we're doing legal?’ and they say, ‘Yes,’ what — am I just supposed to be a lawyer? This is their purpose. . . . It's frustrating to be in trouble for things that you genuinely try to do legally and feel like you went the route you were supposed to to do them legally” (The Tucker Carlson Show).

-

SBF was arrested and jailed in The Bahamas on U.S. criminal charges just one month since FTX’s collapse and the day before he was scheduled to testify about the collapse before Congress, leaving FTX’s bankruptcy CEO, John Ray, to testify unopposed. At least one congressman present thought that “this was a decision made by somebody at DOJ to prevent Sam Bankman-Fried from coming here” (HFSC hearing).

Following extradition to the U.S., SBF was kept under house arrest. In July 2023, he was issued a gag order. Two months before trial, his bail was revoked — apparently with input from the bankruptcy lawyers, as reflected in fee statement entries like “[C]all with N. Roos (SDNY) re: amendment to bail package for S. Bankman-Fried” and “Review and analyze SDNY motion re: bail order . . . Call with SDNY re: S. Bankman-Fried motion . . . Attend hearing re: S. Bankman-Fried bail revocation . . . Review prosecutors’ letter requesting pre-trial detention of S. Bankman-Fried” (second and ninth monthly fee statement of Sullivan & Cromwell).

SBF was jailed on the basis of two alleged attempts at witness tampering:

“[SBF] sent the general counsel of FTX US, who has been referred to as Witness-1, the following message via Signal [and Gmail], an encrypted communications medium: ‘Hey, I know it's been a whole while since we have talked, and I know things have ended up on the wrong foot. I would really love to reconnect and see if there is a way for us to have a constructive relationship, use each other as resources when possible, or at least vet things with each other. I would love to get on a phone call sometime soon and chat.’” (bail revocation hearing). The defense maintained that this was simply “the last of a series of messages that he sent to Witness-1 [and other bankruptcy lawyers] to offer his help supporting FTX’s creditors in the bankruptcy” and that “it was Witness-1 who first reached out to Mr. Bankman-Fried using Signal . . . to encourage him to ‘align’ his efforts to ‘support customer assets’ with efforts by Witness-1 and other in-house FTX attorneys” (court docket).

SBF showed a reporter some private messages from Ellison about how overwhelmed she’d felt at work and how their breakups made things even more difficult. The defense argued that, “The reporter contacted Mr. Bankman-Fried about an article he was already writing that featured Ms. Ellison’s personal diaries and writings. The reporter was already aware of these documents because he had written an article two months earlier in which he described Ms. Ellison’s writings and reported that they contained her ‘raw reflections on SBF’ and her ‘personal and professional resentment’ towards him. Hence, Mr. Bankman-Fried shared copies of writings that the reporter apparently already knew about, and which were not produced in discovery . . . [I]t was a permissible exercise of Mr. Bankman-Fried’s First Amendment right to make fair comment on a media story about himself. . . . The Government [] asserts that because Mr. Bankman-Fried had several phone conversations with the reporter, it has ‘every reason to believe that he was a source for that [earlier] article as well. . . . In fact, it seems apparent that the Government or its agents were the source for at least some of the disclosures to the reporter. The July 20, 2023 article reports that ‘[p]rosecutors are expected to begin preparing at least some witnesses in August, two people with knowledge of the matter said.’ That information could only have come from the Government. . . . Not surprisingly, the published article was unfavorable to Mr. Bankman-Fried and favorable to Ms. Ellison” (court docket).

“The relevant statute,” explained the judge, when remanding SBF to jail, “[says] that whoever knowingly uses intimidation, threatens or corruptly persuades another person, or attempts to do so, with intent to influence, delay, or prevent the testimony of any person in an official proceeding is guilty of a felony” (court docket). And yet the press remained free to vilify SBF without restriction, aided by the government: “[M]ore than 1 million articles mentioning FTX have been published since the bankruptcy. The overwhelming majority of them have been negative towards Mr. Bankman-Fried. The Government is at least partially responsible for this deluge by repeatedly using the press to tout its evidence against Mr. Bankman-Fried” (court docket).

The press was also aided by John Ray. For instance, in an interview released on the first day of the trial proper, Ray said, “[SBF] was involved in everything[ a]nd he took money, and he spent it on stuff that had nothing to do with the business.” He explained that he’d never spoken to SBF because two days into joining FTX, “It’s pretty clear for me what happened in the company and what his role was,” and also explained that he charged creditors $1,300/hour because “[c]rime is very expensive” (Freakonomics). The interviewer offered mild pushback — “[o]ne criticism I’ve heard of your being so public about how poorly the company was run, was that the more chaotic and absurd you can make it sound, the more that it may be to your benefit, to make your role seem even more heroic” — and others noticed the strangeness of Ray’s behavior: “[I]t is hard to think of a CEO in recent memory who has been more focused on trashing the previous management” (Bloomberg).

But Ray continued. In March 2024, he submitted a seven-page diatribe to the court for consideration in SBF’s sentencing, asserting: “Mr. Bankman-Fried continues to live a life of delusion. The ‘business’ he left on November 11, 2022 was neither solvent nor safe. . . . That things that he stole, things he converted into other things, whether they were investments in Bahamas real estate, cryptocurrencies or speculative ventures, were successfully recovered through the enormous efforts of a dedicated group of professionals (a group unfairly maligned by Mr. Bankman-Fried and his supporters) does not mean that things were not stolen. What it means is that we got some of them back. And there are plenty of things we did not get back, like the bribes to Chinese officials or the hundreds of millions of dollars he spent to buy access to or time with celebrities or politicians or investments for which he grossly overpaid having done zero diligence. . . . The remorse is nonexistent. Effective altruism, at least as lived by Samuel Bankman-Fried, was a lie” (court docket).

-

Beyond the issues already discussed, the prosecution’s much-quoted portrayal of FTX as “built on lies” appears to be based largely on: statements about the relationship between FTX and Alameda; SBF’s frequent use of “I don’t recall” under cross-examination; and a tweet thread made to reassure customers as withdrawals spiked.

It’s often claimed that SBF told everyone Alameda’s FTX account was just like everyone else’s, the key reference being a tweet from 2019. But in that tweet, SBF is merely responding to a concern about potential front running: “How are you going to resolve the conflict of interest of running your own derivative exchange, AND actively trading against the market at the same time?” (X). Prosecutors also quoted an email and an interview; SBF claimed the wider conversation in both instances had again been front running. FTX’s former COO told Michael Lewis, “It was literally the first thing I was asked every day. Is Alameda Research front-running us? . . . No one ever asked about liquidation . . . And no one ever asked, ‘Is our money actually inside Alameda?’” (Going Infinite). Wang said front running “was not a thing that happened at FTX, because there was not a way for anybody to see people's orders before they were processed” (trial transcript) and that “Alameda's role as a market maker on FTX was described in documents that FTX put out to the public” (trial transcript) (and in SBF's tweet about front running).

“I don’t recall” was honesty, not evasiveness. “I'm somewhat sympathetic to the idea that being in jail made it difficult for Bankman-Fried to properly prepare for cross-examination” (CoinDesk). “There were around 10 million documents turned over in discovery, not including the database” (Bloomberg). “Bankman-Fried estimated he gave around 50 interviews and didn’t have access to any internal documents. He said he didn’t remember every statement he made to journalists” (CNBC).

As for the tweet thread, “On Nov. 7, 2022, as FTX customer withdrawals spiked, Bankman-Fried wrote: ‘FTX is fine. Assets are fine,’ and that the exchange had ‘enough to cover all client holdings.’ . . . Wang, however, admitted on cross-examination that in a Nov. 17 meeting with prosecutors he said the tweet was true because Bankman-Fried was careful to say that FTX was solvent but not liquid” (Yahoo Finance). “At the point where I posted it,” SBF said, “Alameda still had a net asset value of roughly positive 10 billion. FTX had no holes on its balance sheet. And there had been no attack on the customer assets” (trial transcript). “‘The evening of Nov. 7 and continuing into the morning of Nov. 8, there was a market crash . . . Overall, this led to a roughly 50% crash in Alameda’s assets . . . Alameda was still solvent, but there was little margin for error left.’ . . . Bankman-Fried says that after that, ‘I took down the tweet thread’” (Bloomberg).

-

Some people have doubted the authenticity of SBF’s distinctive look. But not those who have known him the longest, it seems. “The new prime minister arrived . . . Sam emerged, looking as if he had fallen out of a dumpster: cargo shorts, wrinkled T-shirt, droopy white socks. Same guy, thought Ian. From the moment he had started on the project and begun to observe Sam from afar, Ian had found the same thought often crossing his mind: how shockingly just like he’d been in high school Sam still was. When the oddball in your high school class became one of the richest people in the world, you sort of assume the oddball must have changed. Sam hadn’t changed” (Going Infinite).

“[T]he government was able to sell ideas about him that would have struck any of his closest colleagues as preposterous. The suggestion, for example, that everything about Sam’s appearance had been carefully curated to trick people. . . . If Sam Bankman-Fried’s appearance was an act, it was an act he’d performed his entire life. . . . His ‘look’ couldn’t have been more sincere. . . . At some point after he became a public figure — a thing he’d never expected to be — he no doubt noticed that other people seemed to be charmed by his look. His realization would have relieved him of any pressure to alter his appearance. But that’s different from creating a persona to deceive others” (Washington Post).

More significantly, SBF’s demeanor has been used against him as evidence of perjury. A prosecutor told the jury that on the stand, “He had to be asked and reasked[, h]e looked away[, h]e lied about big things, and he lied about little things” (trial transcript), and the judge claimed, “And when he wasn't outright lying, he was often evasive, hairsplitting, dodging questions and trying to get the prosecutor to reword questions in ways that he could answer in ways he thought less harmful than a truthful answer to the question that was posed would have been[;] I've been doing this job for close to 30 years [—] I've never seen a performance quite like that,” (sentencing transcript). The judge also appears to have made his personal interpretations of SBF’s mannerisms plain to the jury:

“It was pretty clear from the judge that the judge did not like him, did he? He really didn’t like his demeanor” (The Rest is Politics)

“Judge Kaplan was visibly irritated with Bankman-Fried, at one point snapping at the FTX founder to ‘just answer the question’” (Protos)

“[SBF] was sometimes chided for straying off topic” (New York Times)

“[Judge Kaplan] was all but openly derisive toward the former crypto mogul when Bankman-Fried testified during the trial itself, to the point where I did genuinely wonder how the jury perceived his comments about the defendant on the stand. Eighteen random members of the public, who had no little or no familiarity with FTX, crypto, Bankman-Fried or being on a jury, may well have easily taken cues from the most visible legal expert who ran the show. . . . Bankman-Fried didn't quite seem to grasp how his demeanor and responses were received by the judge and jury” (CoinDesk)

But as with the crumpled cargo shorts, this was just SBF being SBF. One journalist observed in May 2022, for example, “Bankman-Fried doesn’t mind the question, but he would like it clarified. . . . [SBF] stares fixedly into the ocean . . . By this point he is asking the questions and answering them, and I am just sipping my drink. . . . Bankman-Fried toys with my question as much as he is playing with his salad” (Financial Times). Following FTX’s collapse, however, reporters changed their tone: “Prosecutor calls out Sam Bankman-Fried for fidgeting” (CNBC); “[SBF had] a relatively muted tone, sparse eye contact and lots of details he was never asked to give” (Blockworks); “[SBF] was obviously evading questions, trying to pour forth verbiage to distract Sassoon from what she’d asked” (The Verge).

This conversational style is common among autistic people. “[SBF] has had a diagnosis of ASD that was previously shared with the court. . . . [An autistic person might] be judged to be lying or evasive due to lack of eye contact, or answers that seem non-responsive. . . . [T]hey might repeat themselves or become obsessed on an issue, something we call perseveration. They might become particularly focused on minute details that others find irrelevant, something we call hyperfocus” (disability rights advocate). “[T]ypical diagnostic behaviors . . . can mislead an investigator, attorney, or judge. They may see someone who seems to lack respect and observe a ‘rude, fidgety and belligerent’ person who, by nature of his lack of eye contact and evasive conversation, appears to have something to hide. . . . [You] need to repeat and rephrase questions” (Judge Taylor et al.). The lack of respect for SBF’s neurodivergence may have also caused him to suffer withdrawal during trial: “Bankman-Fried was diagnosed with ADHD and depression years ago . . . [SBF] has been doing his best to remain focused during the trial for the past two weeks, despite not having his prescribed dose of Adderall during trial hours. . . . [His] dose of Adderall in the early mornings . . . would wear off by the time the trial began” (Business Insider).

-

SBF’s “f— regulators” comment is regularly taken out of its context: “f— regulators / they make everything worse / they don't protect customers at all / . . . / it would be good / but regulators can't do it / they can't actually distinguish between good and bad / just ‘do more business’ vs ‘do less business’ and ‘put up more moats’ vs ‘put up fewer moats’” (Vox). SBF expanded on this at trial: “I was somewhat frustrated [and] felt like all the work that I had done to work with regulators might have ended up encouraging bad regulation as much as good regulation in retrospect” (trial transcript).

Furthermore, despite widespread assumptions to the contrary, FTX moved to The Bahamas to pursue regulation — not to avoid it. “[SBF] says they moved to the Bahamas mostly because it was one of a handful of countries that had a ‘full regulatory framework’ for crypto. The Bahamas had been positioning itself at that time as a crypto haven” (Bloomberg). “‘We have been shocked at the ignorance of those who assert that FTX came to the Bahamas because they did not want to submit to regulatory scrutiny,’ said Ryan Pinder, the country's attorney general and Minister of Legal Affairs on Sunday. ‘In fact, the world is full of countries in which there is no legislative or regulatory authority over the crypto and digital asset business, but the Bahamas is not one of these countries’” (TheStreet).

-

“Bankman-Fried says he believed he was permitted to borrow from Alameda as a primary owner. ‘It usually came because there was an investment I needed to make and a I needed capital for, so I would generally borrow funds from Alameda for it,’ he says. ‘It had a few billion dollars of arbitrage-based profit over the prior two years. I saw no reason I couldn’t borrow from it.’ . . . Bankman-Fried says he discussed with lawyers that some people didn’t want the investments to come directly from Alameda. He says attorneys told him an option was to get a loan from the company and make the investment himself. He says lawyers structured the loans” (Bloomberg).

“My personal consumption was a tiny fraction of my earnings, and my consumption, donations, and investments combined were less than—and came from—earnings” (Substack).

-

While SBF did say that “the ethics stuff” was “mostly a front,” he immediately added, “that's not all of it,” and clarified that he thought “ESG has been perverted beyond recognition” and was frustrated was with “this dumb game we woke westerners play where we say all the right shiboleths and so everyone likes us” (Vox). He later elaborated: “[T]here are a lot of things that I think have really a massive impact on the world. And ultimately, that’s what I care about the most. . . . Separately from that, there is a bunch of bullshit that regulated companies do to try and look good. . . . if like three different quarterbacks throw a touchdown in the same game for the same team, we will donate two used cars to charity-type campaigns. . . . We thought about ourselves as legitimately trying to do good, but we also thought about what we could do to make sure that our image reflected that” (New York Times). Luxury cars, for instance, would not have reflected a legitimate desire to do good: “I bought [SBF] a BMW to drive around in and he made me sell it and get him a Corolla” (X).

Much attention has been given to FTX’s spending on lavish real estate and marketing. But perhaps the property was simply “sound real-estate investments, and Bankman-Fried needed fitting places to host such figures as Bill Clinton and Tony Blair . . . In a widely amplified story, Fox Business reported that Bankman-Fried owned a yacht; the claim was attributed to a local yachtsman, who said he frequently spotted Bankman-Fried at the marina, and Bankman-Fried’s spokesman categorically denied that his client had himself ever ‘owned’ a boat” (New Yorker). The defense emphasized that “‘the Bahamas real estate was corporate housing for FTX employees.’ FTX, he said, was trying to court top professionals who ‘uprooted their lives’ to move there when they could just have easily gone to work at Google or Facebook” (Guardian). A co-defendant revealed that “Sbf hated flying private” (X) and “hated the penthouse it just had the right number of bedrooms” (SBF and nine roommates rented it from FTX) (X); he also explained that “there's [only] two types of real estate” in The Bahamas — “this ultra wealthy section” and “the impoverished section” (The Tucker Carlson Show). As for the marketing, “‘When I looked into competitors’ marketing budgets, they appeared to be 100% of the revenue,’ Bankman-Fried says. ‘We were spending 10 to 20% on marketing’ . . . Multiple crypto companies . . . ran Super Bowl ads” (Bloomberg). Far from the jet-setting life of luxury often portrayed, SBF “didn’t drink or party” (TIME), “worked 12 to 22 hours a day, and took one day off every couple of months” (The Verge), and never set foot on the “semi-private beach” beneath the penthouse (Going Infinite).

SBF has also been criticized for only donating $190 million to nonprofits in 2022. But an advisor to the FTX Foundation says that they “got a lot of criticism for scaling up giving too quickly — so going from zero to one to two hundred million in a year is a very big scale-up and is actually just quite hard to do . . . [and] the way it seemed to me at the time, and I guess still does just seem to me, was basically consistent with someone trying to scale up their giving as fast as they can, and in fact . . . plausibly he should have been paying more attention to the business and not getting distracted by other things” (Making Sense with Sam Harris).

According to SBF’s psychiatrist, “Sam is on the autism spectrum,” which has “impaired his ability to communicate emotions” (George Lerner), a phenomenon known as alexithymia. This may explain comments like “There’s a pretty decent argument that my empathy is fake, my feelings are fake, my facial reactions are fake” (The Block). If an autistic person regularly feels the need to fake emotion to fit in, that doesn’t mean they’re not motivated to help others.

To the contrary, letters to the court detail a long history of altruism (court docket): SBF’s executive assistant says he “never acted out of greed or self-interest” and that he “consistently demonstrated a commitment to ethical business practices and a genuine desire to make a positive impact on the world”; a Rwandan charity advisor comments on how SBF was “well-informed of Africa’s unique challenges” and lamented how much the media coverage was “littered with claims I knew were false”; a crypto skeptic suggests this is “the first time in the entire history of criminal justice where the defendant donated most of his earnings at his previous job to charity”; an FTX victim notes how SBF “cared about chickens in university” even though “people hate animal rights activists”; and SBF’s family write, “he has never felt happiness or pleasure in his life and does not think he is capable of feeling it” and “He wouldn’t make small talk about your dog, but he’d subsist on bread and water in prison to avoid eating an animal. He was never good at apologizing, but always quick to admit fault. He would be uncomfortable giving me a hug, but I know he would give me a kidney if I needed one.”

-

“[SBF] has shown an immense amount of remorse and regret for whatever mistakes he made . . . I am not use to this; every other person that I have interacted with here places the blame on someone else” (ex-NYPD cellmate).

“I should have been on top of this and I feel really, really bad and regretful that I wasn’t and a lot of people got hurt and that’s on me” (Forbes). “I was C.E.O. of FTX, and that means whatever happened, why ever it happened—I had a duty. I had a duty to all of our stakeholders, to our customers, our creditors. I had a duty to our employees, to our investors and to the regulators of the world to do right by them and make sure the right things happened at the company. And clearly, I did not do a good job with that. Clearly I made a lot of mistakes. There are things I would give anything to be able to do over again. I did not ever try to commit fraud on anyone” (New York Times).

“‘I'm haunted, every day, by what was lost . . . It's most of what I think about each day . . . I never thought that what I was doing was illegal. But I tried to hold myself to a high standard, and I certainly didn't meet that standard’ . . . Bankman-Fried said Sunday that ‘of course’ he is remorseful. ‘I've heard and seen the despair, frustration and sense of betrayal from thousands of customers; they deserve to be paid in full, at current price,’ he said. . . . He added that he ‘felt the pain’ from co-workers as he ‘threw away what they poured their lives into’ and from the charities he supported ‘as their funding turned into nothing but reputational damage. . . . I never intended to hurt anyone or take anyone's money. But I was the CEO of FTX, I was responsible for what happened to the company, and when you're responsible it doesn't matter why it goes bad. I'd give anything to be able to help repair even part of the damage. I'm doing what I can from prison, but it's deeply frustrating not to be able to do more,’ he said” (ABC News).

“Sam Bankman-Fried was never presumed innocent. He was presumed guilty—before he was even charged. He was presumed guilty by the media. He was presumed guilty by the FTX debtor estate and its lawyers. He was presumed guilty by federal prosecutors eager for quick headlines. And he was presumed guilty by the judge who presided over his trial.”

❖ THE BIG PICTURE ❖

It’s easy to forget what we would have expected to see, but didn’t

Prosecutors claimed that their witnesses “stole customer money at the defendant's direction” (trial transcript). And yet “none of [said witnesses] testified that he told them to steal money or commit crimes” (Quartz). More broadly, “none of the witnesses at this trial testified that Sam told them or directed them to violate the law or said or did anything that showed he thought he was violating the law” (trial transcript). Neither could the prosecution produce any other evidence to this effect, despite extensive access to — and help investigating — FTX’s people and data: “[W]e would do whatever the Government requested relative to cooperation. . . . [such as providing] full access to the information on a real time basis . . . We’ve provided an analysis of several hundred thousand documents. We’ve interviewed and received proffers of 24 current and former employees” (John Ray, bankruptcy hearing). (The defense, on the other hand, was not so fortunate.)

“If Bankman-Fried were such a criminal mastermind, Cohen asked the jurors, ‘why would he go before Congress and subject himself to public questioning? . . . These were extremely wealthy people’ who could have, at any time between 2020 and 2022, when the alleged crimes were happening, taken their money and run. They could have cashed out, notified authorities, hired lawyers. But none of them did, Cohen said. Because in the moment, ‘they don’t think they’re doing anything wrong’” (CNN).

Even in the period between FTX’s collapse and SBF’s arrest, “[d]uring those five weeks, as far as I am aware Sam was free to leave the Bahamas for a jurisdiction without an extradition treaty with the US . . . He was resolute that he would not leave as long as he thought he could do some good by staying . . . He had no patience for conversations about defending himself” (ex-Head of Data Science at FTX).

The justice system is vulnerable to abuse

Why did SBF’s colleagues plead guilty and testify against him? According to prosecutors, they “agreed to testify in the hope of receiving a shorter sentence” (trial transcript). But they may have also pled guilty out of self-interest regardless of whether or not they were, in fact, guilty.

The prosecutor has more control over life, liberty, and reputation than any other person in America. . . . He can have citizens investigated . . . to the tune of public statements and veiled or unveiled intimations. Or the prosecutor may choose a more subtle course and simply have a citizen’s friends interviewed. The prosecutor can order arrests, present cases to the grand jury in secret session, and on the basis of his one-sided presentation of the facts, can cause the citizen to be indicted and held for trial. . . . [A] prosecutor stands a fair chance of finding at least a technical violation of some act on the part of almost anyone. In such a case, it is not a question of discovering the commission of a crime and then looking for the man who has committed it, it is a question of picking the man and then searching the law books, or putting investigators to work, to pin some offense on him. . . . [T]he real crime becomes that of being unpopular with the predominant or governing group, being attached to the wrong political views, or being personally obnoxious”

— Robert H. Jackson, Attorney General of the Unites States (1940-1941)

One co-defendant, however, refused to testify against SBF, later calling the trial “one sided coerced legal theater provided by people willing to say anything to stay out of prison[, m]uch of it not rooted in reality” (X). Regretfully, he also let fear of retribution from the DOJ prevent him from testifying in SBF’s defense, and said that “a lot of people aren't speaking up about the FTX situation because they're still waiting to settle with the bankruptcy estate” (The Tucker Carlson Show). The estate, allegedly, “worked hand-in-glove with the prosecutors to charge and imprison Bankman-Fried, in ways that far exceeded normal ‘cooperation’” (SBF’s appeal).

According to Michael Lewis, some witnesses for the prosecution thought SBF was innocent: “I saw the prosecutor's list of witnesses, and it maps on to the characters in the book in the most extraordinary way. . . . And I'm in touch with most of these characters. I've been interviewing them since it all fell apart. And they've told me what they're going to say, and some of them have said to me, I think Sam is innocent” (Washington Post).

Was this trial ever about justice — or was it about politics?

CRYPTO GOES ON TRIAL ALONGSIDE SBF

When a major company implodes, there’s always pressure to find a villain; understandably, the CEO becomes the lightning rod by default. In the case of FTX, that CEO also happened to be the ‘white knight’ of a sector the U.S. government had begun to wage war on. Yes, he’d been a top Democratic donor, but it was just coming to light that he’d been giving similar amounts in dark money to Republicans. The political calculus had shifted. (The DOJ’s press release following SBF’s sentencing suggests this was still a sore point more than a year later — he hadn’t been convicted of a campaign finance charge, yet the statement claimed he “took FTX customer funds for . . . millions of dollars of political contributions to candidates from both parties.”)

From the moment SBF handed control of FTX to his lawyers, the narrative was locked in: Crypto’s poster boy had squandered billions of his customers’ money gambling on sh*tcoins and partying with celebrities in the Caribbean! The ‘quirky, genius philanthropist’ persona was all a con! Never mind those technical details like ‘peer-to-peer margin lending’ or ‘illiquid but solvent,’ or the challenges of trying to innovate in a regulatory gray zone — in the confident words of the U.S. Attorney for S.D.N.Y. one month later, “this was not a case of mismanagement or poor oversight, but of intentional fraud, plain and simple” (DOJ website).

Or so we were told, anyway.

The Department of Justice is not a digital assets regulator. However, the prior Administration used the Justice Department to pursue a reckless strategy of regulation by prosecution, which was ill conceived and poorly executed.

SBF was a proxy for a movement that threatened entrenched financial interests. His 25-year sentence was a warning. A shot across the bow of an industry built on decentralization, transparency, and autonomy. When the jury reached their verdict, the U.S. Attorney General announced, “This case should send a clear message to anyone who tries to hide their crimes behind a shiny new thing” (DOJ website). Perhaps the administration’s real message was simply “to anyone who tries . . . a shiny new thing.”

In the end, it wasn’t just SBF’s freedom on the line, but also the reputation of an entire industry. And the verdict reverberates far beyond a Manhattan courtroom.

WHAT NOW?

On November 4, 2025, a three-judge panel heard SBF’s appeal. The panel will likely decide whether to grant a retrial in early 2026.